- The Evolved Investor

- Posts

- Creative Destruction on Steroids

Creative Destruction on Steroids

Accelerating technological disruption means increased investor risk

ICYMI: There’s a revolution going on at Chili’s

Brinker International Inc. (NYSE: EAT), the parent company of Chili’s Bar and Grill and Maggiano’s Little Italy restaurants, has been experiencing a major comeback. The stock has been propelled by higher revenues and profitability driven by a more streamlined menu, inexpensive items, and improved customer experience, all fueled by GenZ viral TikTok videos. In the past year, the share price has gone from $43.25 to $161.00, representing a 250%+ return. That’s some cheese pull!

CEO Kevin Hochman, who came to Brinker from KFC in 2022, dismissed concerns that competitors Applebee’s and Red Robin:

"I said, 'Are you guys worried about that number, the $9.99?' And they all just started laughing," he said. "I was like, 'Why are you guys laughing?' And it's like, because we know how strong [we are]. We've been in the gym, we've been working out, and we are not afraid of competitors undercutting us. I think that's what you're seeing in these results."

Schumpeter’s concept meets AI

Austrian economist Joseph Schumpeter introduced the concept of “creative destruction” in his 1942 book Capitalism, Socialism, and Democracy. The idea seems simple today: innovations will displace existing business models. Think of how the rise of mobile phones has made phone booths obsolete: Netflix replaced Blockbuster, Spotify replaced Sam Goody and Tower Records, and Amazon has largely replaced Toys R’ Us and other retailers as the go-to for higher margin items.

This has always been the case, yet what is different today is the rate at which technological advancements are making existing business models inherently riskier. The Evolved Investor must not only seek to determine if there is significant value in a company’s predicted future cash flows relative to its current price, but they must also qualitatively assess the threat to those predicted cashflows in the face of technological disruption. From the 1950s until the early 2000s, most companies operated with the same technological constraints: compute power, robotics, manufacturing innovations, and process improvement. Today, technologies like machine learning, artificial intelligence, blockchain, and quantum computing are unlocking tidal waves of innovation that may destroy existing business models.

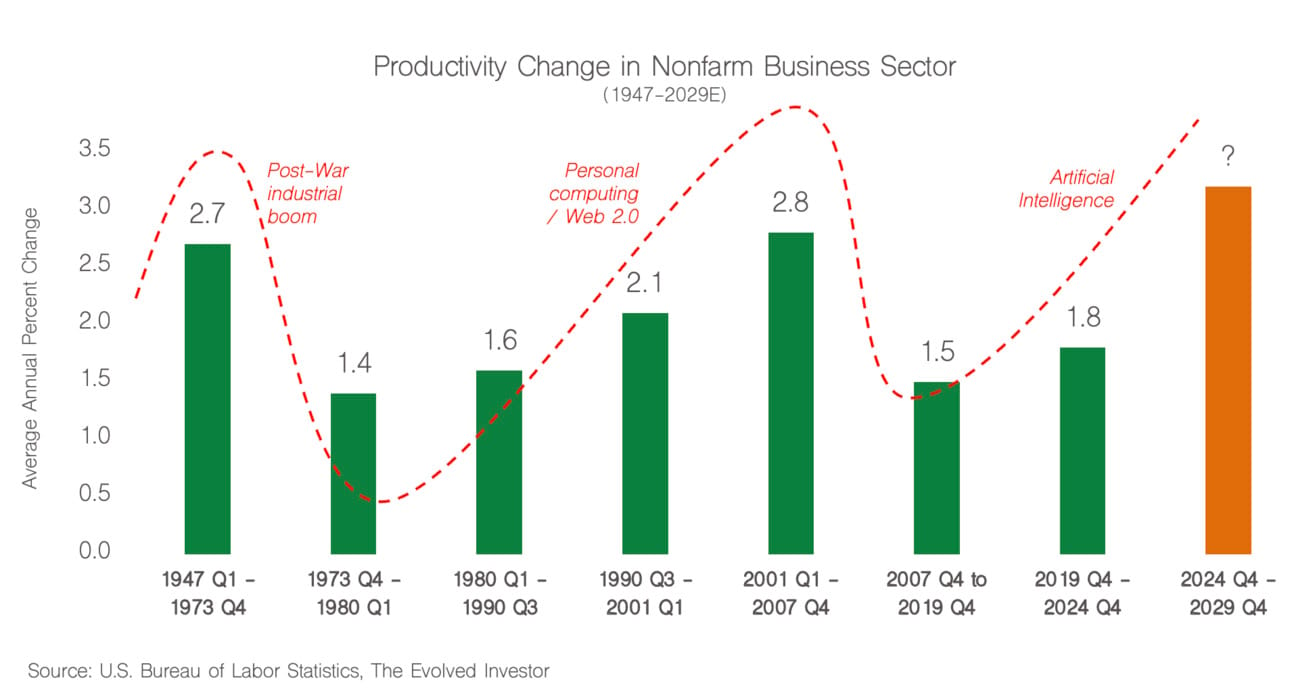

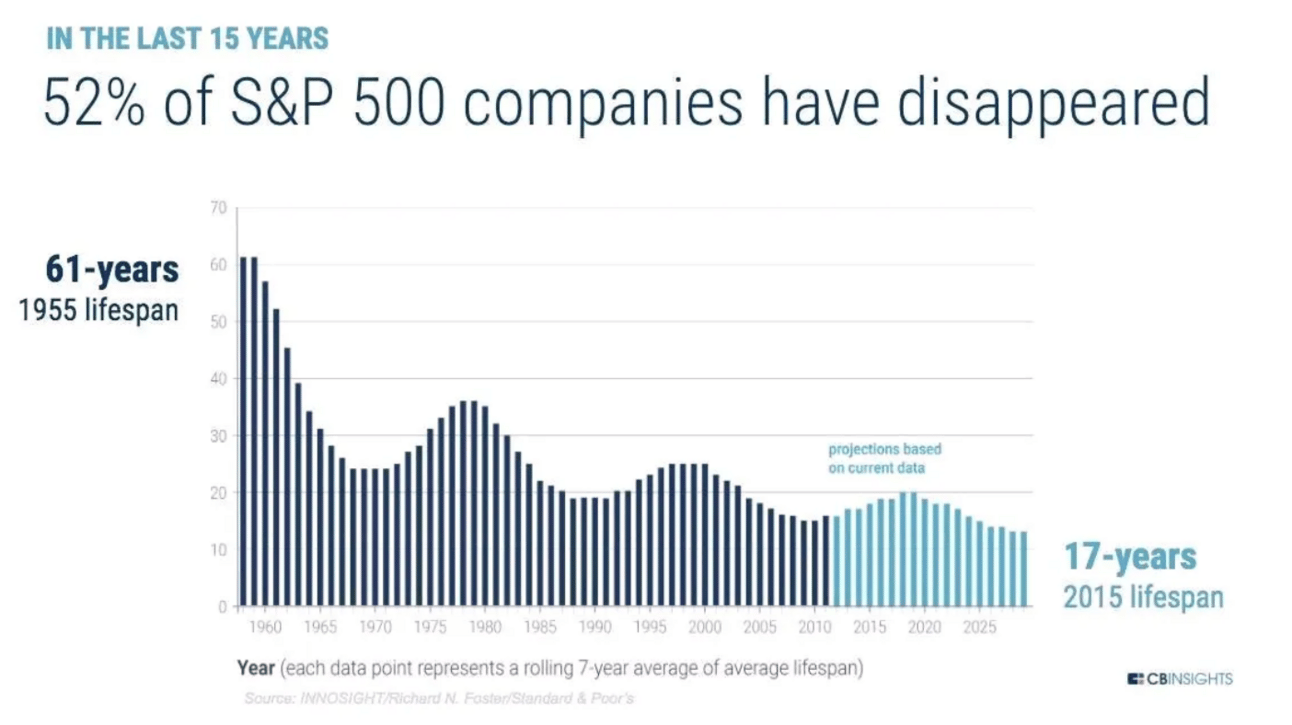

Although it is difficult to measure the intangible effects of accelerated technological change directly, we can see anecdotal evidence in the form of increased productivity, as shown in the graph above, as well as the shortened lifespan of large companies. The graph below demonstrates that over half of the S&P 500 companies have disappeared in the past 15 years. However, while it is true that some of these have been due to acquisition or private equity buyouts, where investors were paid for their invested capital, it also signals that creative destruction, driven by rapid technological advancement, is likely accelerating the lifecycle of a large company.

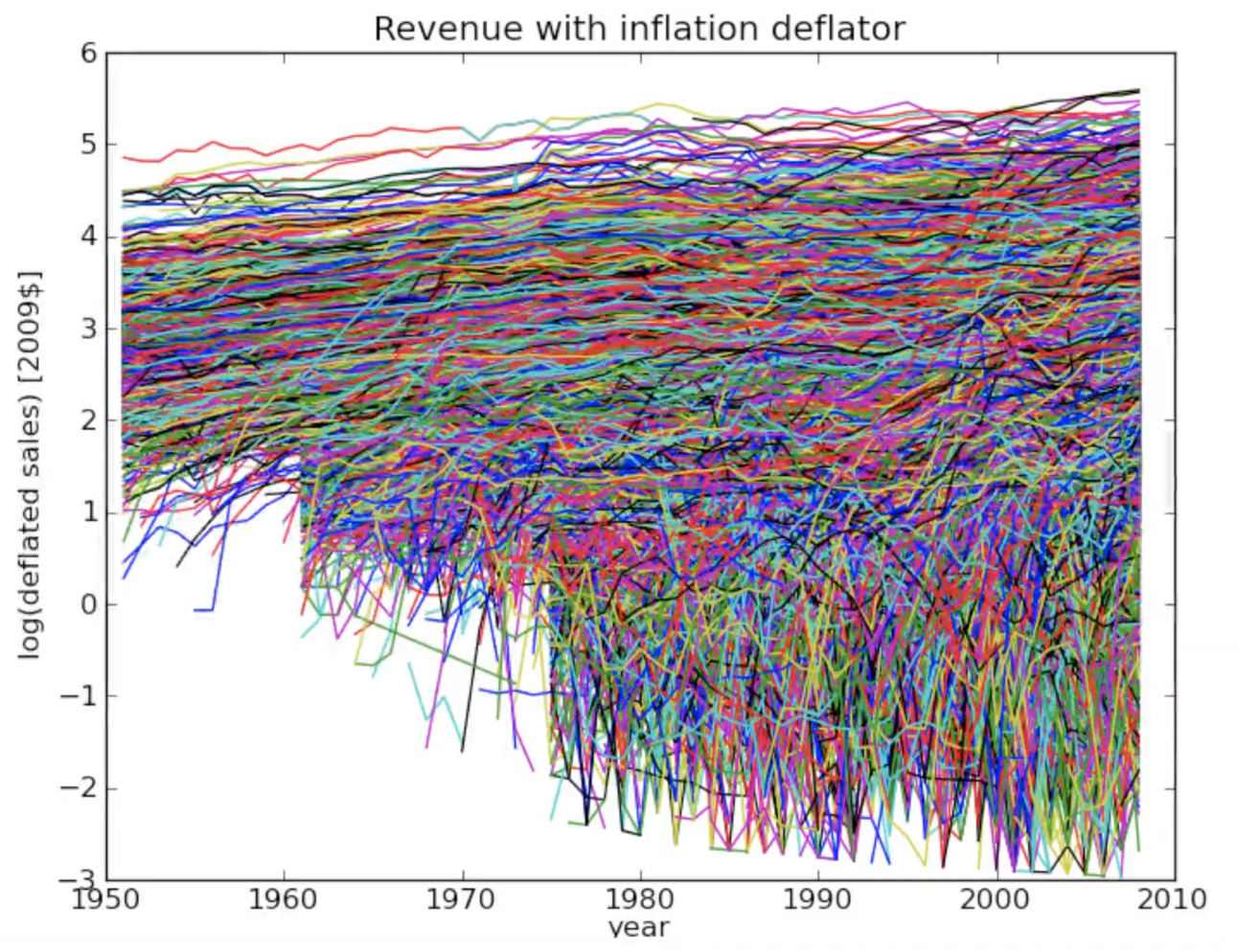

In a 2011 TEDTalk, physicist Geoffrey West outlined the link between the growth and behavior of cities and companies and how both of those entities mimic many of the laws of conservation and metabolism observed in biology. What was interesting to note was that toward the very end of the talk, he had a few graphs outlining how companies grow in a sigmoidal fashion — with an exponentially increasing speed at first (i.e., hockey stick growth) — which then tends to diminish over time and eventually stalls out until the company is no longer relevant. Very few companies can resist this “natural” tendency, as he shows in this eye-popping chart below.

Source: The Surprising Math of Cities and Corporations, Geoffrey West

As Professor West stated so summarily in his talk:

“They they are, that’s 23,000 companies. They all start looking like hockey sticks, they all bend over, and they all die, like you and me.”

Evolved Investors would be wise to understand the scope of technologies that could play a role in accelerating this process in the companies they select and perhaps re-evaluate their time horizons from “hold for forever” to something more medium-term vs. long-term.

Sponsored Post

Visa (V)

We like Visa for many reasons, but mainly its strong market position and its ability to grow cashflows over time. Visa’s ROIC has remained above 18% since 2018 and has been increasing, approaching 30% as of the end of calendar year 2024.

Visa’s brand is universally well known and trusted brand, its “everywhere you want to be” network gives it a competitive advantage, and is well positioned to capture more market share as the secular trend to digital payments continues globally. Visa’s payments volume in 2023 of $12,620 billion was larger than all of its competitors combined (page 26).

On the financial side, there is also a lot to like. Increased revenue, net income, and EBITDA and it’s hedged against inflation since payments volume will have the underlying pricing built in.

There’s a famous Warren Buffet quote: “I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.” We certainly are not insinuating that CEO Ryan McInerney is nothing but a brilliant, hard-working, and solid steward for the business, but rather that the Visa business is “so wonderful,” it would be difficult to derail the momentum.

The valuation is the only holdup for us for a Strong Buy right now. Sitting at a PE ratio of around 35, we suggest keeping this on the radar. During a broad market correction or downturn, closer to a PE ratio of 25 would be a safer bet, with all other factors held constant. Definitely a company to keep on your radar.

Did a friend send you this newsletter? Sign up here to get weekly news and bespoke value investing content to make informed decisions about your portfolio.

Want to advertise with us? Please send us a note at [email protected]

Legal Disclaimer: The Evolved Investor is for information purposes only and is, by law, not personal investment advice. Concepts and ideas are for your consideration only. We encourage our readers to do their due diligence. Investing has inherent risk, and investments can lose value.