- The Evolved Investor

- Posts

- Caveat emptor!

Caveat emptor!

Rich valuations in a landscape of cheap money

Fear itself

In March of 1933, amid the Great Depression, FDR famously used the platform of his inaugural address to urge Americans to take action. Remembered for his famous line, “The only thing we have to fear is fear itself,” the speech was part of an effort to jumpstart the recovery. Nearly a century later, the LA Times reports that US consumers are becoming more pessimistic about the economy, citing inflation and tariffs. At the same time, many Federal workers and Federal contractors are either losing their jobs or fearing for their careers as DOGE continues its sweeping and unprecedented firings across the public sector.

The impact of hundreds of thousands of workers losing their income source over the coming months, combined with rising costs, will put tremendous strain on many American households. Additionally, US companies providing goods and services to those households will see a decrease in aggregate demand. Rather than quelling fear and fostering price stability and wage growth, the actions of the new Administration are increasing levels of risk and uncertainty in the markets under the pretense of improving efficiency.

Stock Valuations and the Money Supply

In school, we all learned a bit about inflation, the experience of the Weimar Republic, and perhaps the hyperinflation scenario in Zimbabwe. When a government is mismanaged and can no longer borrow, sometimes leaders think they can print their way out of problems. Historically, that has always caused major issues: prices for domestic goods rise more quickly than wages, a lack of trust in the local currency materializes, and people shift their wealth into alternative currencies or invest in physical assets like real estate or precious metals like gold.

Recently in the United States, two major events, the Great Financial Crisis (GFC) of 2008-09 and the COVID-19 pandemic, have triggered the Federal Reserve to use its power to “fix” the economy. Proponents of a theory dubbed “Modern Monetary Theory” emerged claiming that the Fed could simply print its way out of problems ranging from eliminating poverty to providing a safety net to combat the effects of technological change on the labor force — remember one-time Presidential candidate Andrew Yang’s plan for a Universal Basic Income (UBI)? There was not, of course, a lot of explanatory evidence of why this theory would hold and why this time, in a modern era, the same kind of inflation that had triggered catastrophic problems in the past would not be manifested.

The major problem during the COVID response was exactly how much liquidity — excess capital — was injected into the system and to which areas of the economy it went:

During the pandemic, pockets of the economy were impacted more severely like restaurants, retail, hospitality, and transportation. For the most part, Other sectors remained relatively untouched. Most office workers simply started working remotely, and essential workers in hospitals, police, factories, schools, and construction continued to operate with enhanced safety protocols.

The Federal government's response to help the displaced workers was ill-designed and poorly executed. Instead of targeting those whose incomes disappeared overnight, which was the goal of the $837B March 2020 CARES Act. Congress then passed the Paycheck Protection Program (PPP) costing $410B, then added $2,300B in December 2020, and voted finally passing the $1,900B American Rescue Plan in April 2021. All together, COVID-19 funding was approximately $5.5 TRILLION, which included stimulus checks that went out to virtually every American not just those affected by income loss and additional child credits of $3,000 per child even if their parents’ income was unaffected by the pandemic. Many workers who worked from home saw increases in their real income as they saved on commuting expenses like tolls, parking, and public transit passes as well as dining and vacation options.

To make matters worse, the government also gave small businesses access to PPP loans which many businesses took, even though their business model was unaffected by the pandemic, think of a small investment management firm or dentist office with a staff of less than 20 employees. Those “small businesses” were still earning the same revenue as they were before the pandemic, but were able to take government loans, most of which, former Treasury Secretary Mnuchin, declared they would not track down or enforce repayment of. Quiet simply, it was the largest most corrupt transfer of wealth from the working class to the wealthy class in American history.

Well, where did all that government money — from the American taxpayers both present and future — go? Some of it went to pay down debt, but since most of the funds went to wealthier households, it went into buying assets. As the money supply grew to historical levels, it didn’t take long for the price of everything, especially real estate and the stock market to rise to historically rich levels. If you thought MMT was a good idea five years ago, you are seeing it in action today, and how it has negatively distorted the economy and not helped average Americans get ahead.

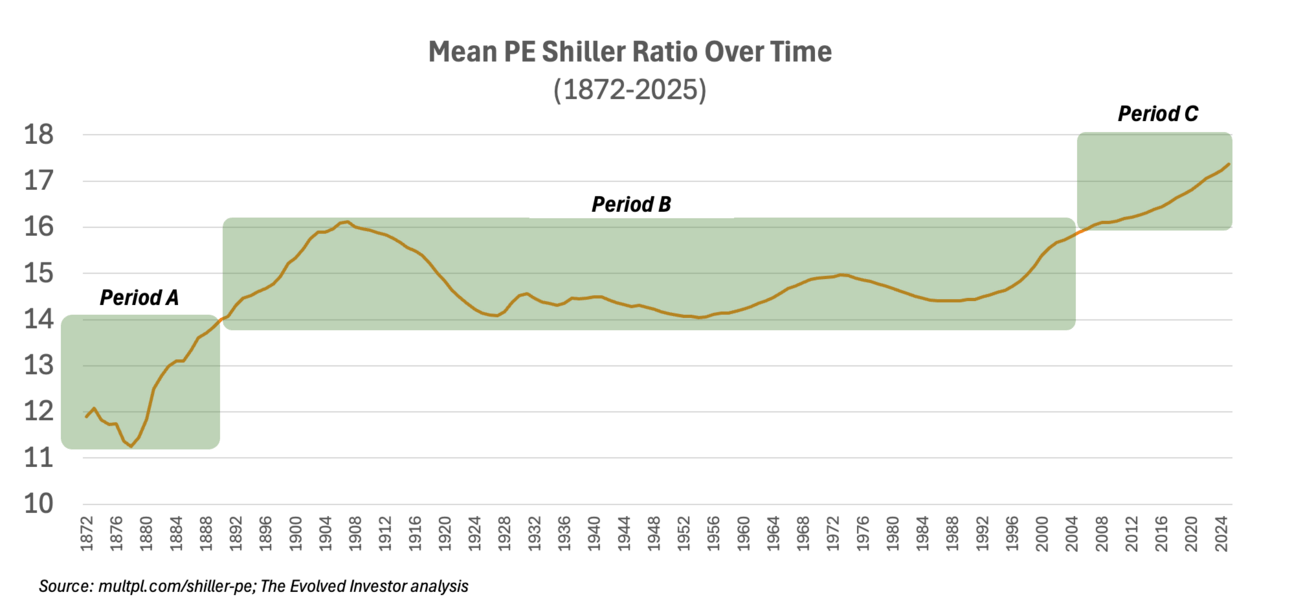

As we think about PE ratios from an investment perspective, note that the mean Schiller PE ratio going back to 1872 used to stand at around 15 for almost the entirety of the history of the stock market (Period B), except for the “startup phase” Period A, where the stock market as a concept was still gaining traction. Since the spike in the money supply in 2020 relative to the size of the economy, the mean has risen above 17 — a 180 basis point increase — in only 25 years. So now we’re in this “Period C”, and we at The Evolved Investor are not as optimistic about Ray Dalio’s idea of a “beautiful deleveraging” coming to fruition and thus assume that the money supply will remain similar to its current inflated levels of the foreseeable future. Coupled with looming tariffs and DOGE-induced unemployment expected to wreak havoc on the economy, now, more than ever, defensive stocks with a value-oriented disposition have the potential to yield superior returns in a long-run time horizon and mitigate any short-term losses.

Sponsored Post

MCO

Moody’s is a credit rating agency and financial services company. Along with Fitch Ratings and S&P Global, one of our previous stock ideas, Moody’s enjoys a solid protective moat from competitive forces.

Performance has been consistent and strong historically: For 2024, revenue was up 13%, net income 16%, and profit margins are very healthy, with an EBITDA margin of just over 43%. Additionally, MCO has a small dividend — yield of 0.75% — and $1.6B in share repurchase authorization going into 2025. Historically, the firm boasts a strong track record of ROIC.

We have been discussing high valuations, MCO currently trades at a current PE ratio of around 44, higher than the entire market mean, which itself is at historical highs. From a valuation perspective, MCO is not trading at an attractive price currently. The MCO CEO has been slowly unwinding his position, selling $135K chunks roughly every two weeks, in a sign that perhaps he knows the valuation is rich.

We recommend keeping MCO on your tracker and consider taking a position after a significant broad market correction brings the valuation in line with future cashflow potential. This is a great company at an okay-to-bad price, if the price goes down significantly, this could be an amazing pickup.

Did a friend send you this newsletter? Sign up here to get weekly news and bespoke value investing content to make informed decisions about your portfolio.

Want to advertise with us? Please send us a note at [email protected]

Legal Disclaimer: The Evolved Investor is for information purposes only and is, by law, not personal investment advice. Concepts and ideas are for your consideration only. We encourage our readers to do their due diligence. Investing has inherent risk, and investments can lose value.